On July 1, unregistered NDIS providers will no longer receive their payments for legitimate claims on behalf of clients. Many are ill-prepared. Claudia Weisenberger reports.

For thirteen years, the National Disability Insurance Agency (NDIA, which manages the NDIS scheme) has allowed so-called ‘platform operators’ and Supported Independent Living Providers to bill them without being formally registered. On July 1 this year, that will stop, and thousands of providers have been given little notice.

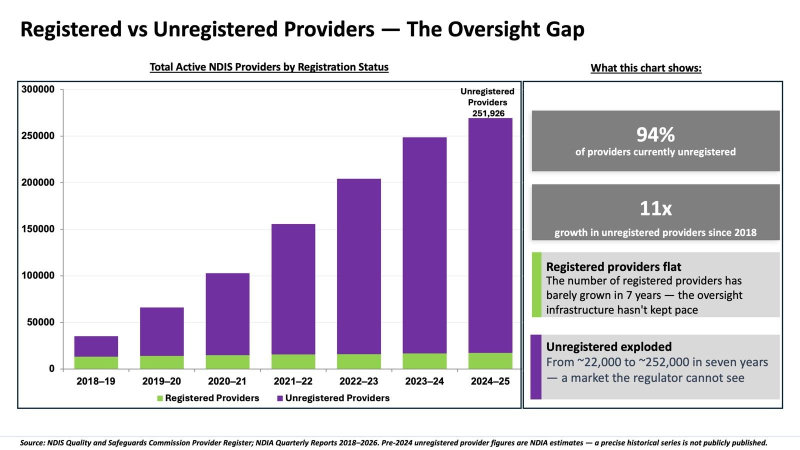

Today, 94% of active NDIS providers are unregistered.

Of more than 274,000 active providers, only 17,374 hold formal registration with the NDIS Quality and Safeguards Commission. The other 257,000 operate without audit, without practice standards review, and without the compliance obligations that registration has required.

A decade of neglect

Since the NDIS was launched in 2013, the scheme has operated on a foundational design choice that few outside the sector understood: the overwhelming majority of providers have never needed to register.

This was a deliberate policy decision. Unregistered providers could deliver support only to participants who self-managed or used plan managers — a large and growing segment of the scheme.

One consequence is

94% of NDIS providers have also never been audited. Not once. In thirteen years.

The result is a market in which the regulated minority of NDIS providers operate alongside an unregulated majority, where the NDIA has limited systematic visibility of what most of the scheme’s providers are actually providing.

It comes on top of the proposed legislation, which will see up to 300,000 people removed from the NDIS entirely. The proposal is being fiercely opposed by the disability community.

Leakage vs fraud

One of the arguments used for the necessity of changes to the NDIS scheme is the magnitude of fraud and over-charging (leakage).

However, in May 2026, John Dardo, NDIA’s Integrity Transformation Chief and co-chair of the government’s Fraud Fusion Taskforce, appeared before a parliamentary inquiry and confirmed what many in the sector had long suspected:

There is no statistically valid way to measure how much leakage is due to fraud.

What Dardo could confirm was a total figure: integrity leakage — a term the NDIA uses to cover criminal fraud, incorrect claims, poor record-keeping, misunderstanding of rules, inappropriate claiming and other non-compliance — accounting for approximately 8.3% of total NDIS payments, roughly $3.7B last financial year, and growing in line with a scheme now forecast to cost approximately $54B annually.

It is important to be precise about what that figure means. Integrity leakage is not a synonym for fraud.

It covers criminal fraud, administrative error, billing mistakes and compliance failures combined. By Dardo’s own admission under parliamentary oath, the NDIA cannot tell you what proportion is deliberate crime and what proportion is an honest mistake. That is precisely the measurement problem.

To put that in context: fraud across all other federal government programs runs at less than 1%. The NDIS figure is more than eight times higher.

The unregistered provider market is not solely responsible for that gap. But it provides the structural conditions that make large-scale exploitation possible: no audits, no practice standards,

no systematic oversight of what is claimed versus what is delivered.

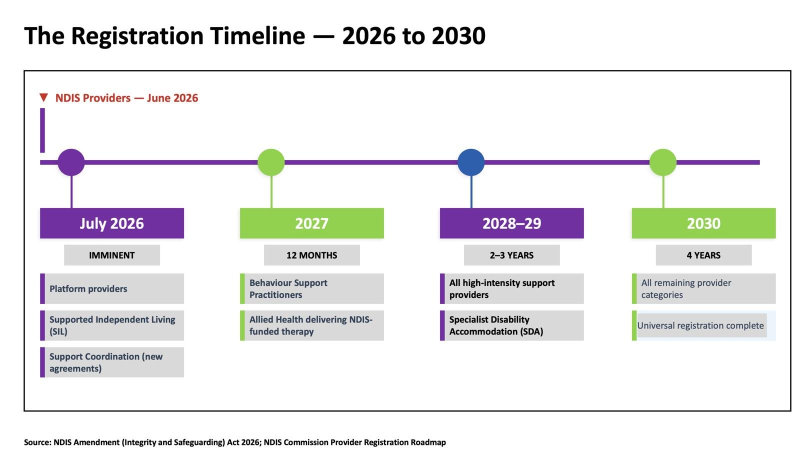

What changes on July 1?

The NDIS Amendment (Integrity and Safeguarding) Act 2026, which received Royal Assent in April, introduces phased mandatory registration. The first categories affected from 1st July are:

- Platform providers — digital apps and websites connecting participants with support workers

- Supported Independent Living (SIL) providers — regardless of how participants manage their plans

- Support Coordination providers — for all new service agreements

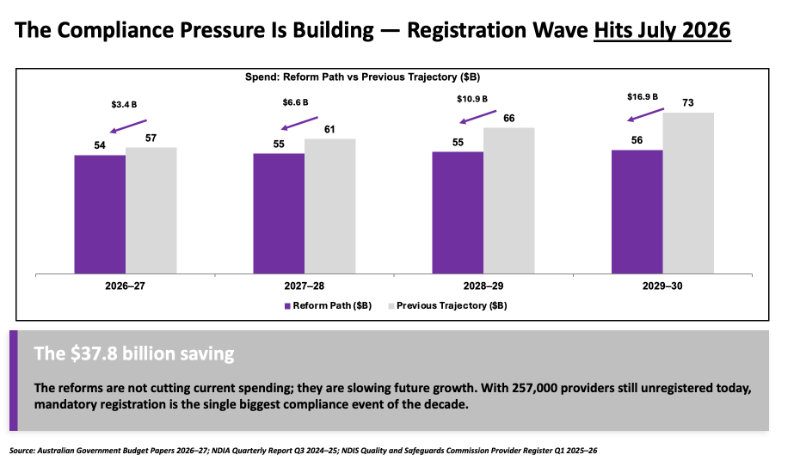

A broader mandatory registration program will progressively extend to all provider categories through to 2030, backed by $1.4B in additional integrity funding.

The registration process is not fast. Applications, audits and worker screening clearances typically take three to six months. The government announced the July 2026 deadline in December 2025, leaving approximately six months for affected providers to comply. Barely enough for most and not nearly enough for many.

Nevertheless, from 1 July, the NDIA’s automated claims validation system will cross-reference every claim against provider registration status in real time. Claims from unregistered SIL and platform providers will initially be rejected and, at best, delayed.

The mandatory registration program is perhaps the most significant improvement in provider oversight since the program’s inception, but the rush to implement it may prove catastrophic.

The July 2026 deadline covers only three categories, however. The remaining provider categories, the overwhelming majority, will have several years to comply.

In the interim, the Fraud Fusion Taskforce — 24 government agencies sharing financial intelligence — continues to operate primarily as a post-payment recovery mechanism. Money leaves the scheme, investigations are launched, and prosecutions follow years later. The taskforce has confirmed more than 660 active investigations and blocked $86m in suspicious claims in 2024-25.

Against $4.5B in estimated annual leakage at the current forecast spend, $86m blocked represents less than 2 cents in every leaking dollar.

The government’s own data suggests the gap between what is being caught and what is being lost remains vast — and the structural conditions that enable it will

not be fully addressed until universal registration is complete in 2030.

For providers in the affected categories who have not yet begun the registration process, the message from 1st July is unambiguous: the system will not wait. The scheme that once asked very little of most of its providers now demands accountability.

Registration is necessary, but it’s not the only reform needed. The July 2026 reforms close the gap for unregistered operators. What they cannot do is guarantee that registered providers behave with integrity. That requires pre-payment verification infrastructure, benchmark data, claims validation, and anomaly detection.

More on that later.