Lingering conflict in the Middle East could cause Australia’s economy to briefly contract and unemployment to spike to pre-pandemic levels, Treasury warns in the nation’s fiscal blueprint.

While Treasurer Jim Chalmers said Australia was well placed to weather headwinds blowing in from the Strait of Hormuz as he released his fifth budget on Tuesday night, he acknowledged households and business could be hit hard by a prolonged war.

Under a severe downside scenario prepared by Treasury boffins for the budget, oil prices were assumed to rise from about $US104 a barrel to as high as $US200 a barrel, with corresponding price increases for other commodities like fertiliser.

In that scenario, Australia’s economy would only narrowly avoid a recession – which is two consecutive quarters of negative growth – but still shrink in the September quarter.

Annual GDP growth would fall from 2.6 per cent currently to 1.25 per cent in 2026/27, 0.5 per cent lower than forecast in Treasury’s base case.

Yearly inflation would peak at around 7.25 per cent in December and unemployment would hit five per cent in 2027/28.

“Price pressures stemming from the conflict are expected to broaden in the coming months, as price increases for petroleum-dependent products are passed through supply chains,” the budget warned.

That would have significant consequences for households and businesses already reeling from three straight Reserve Bank rate hikes.

Higher cost pressures will squeeze business margins and threaten viability, the budget warned.

Dr Chalmers said Australia was better placed and better prepared than most countries to deal with the global crisis.

“As Australians, we confront these serious challenges together from a position of strength,” he said in a speech in Parliament House.

Economists warned that a budget spending splash could further exacerbate inflation, already at 4.6 per cent, by adding to the demand at a time when the economy is already supply-constrained.

Dr Chalmers touted his government’s efforts to drive down real spending growth, which is now forecast to fall from 4.3 per cent in the current financial year to 1.3 per cent in 2026/27 and 0.7 per cent in 2027/28.

”We are playing a helpful rather than a harmful role in the fight against inflation,” he told reporters.

Still, the fall in real spending growth is largely due to a surge in inflation.

Payments as a percentage of GDP are set to rise to 26.8 per cent in 2026/27, which is the highest ratio since 1987, excluding the COVID-19 pandemic.

At the centre of the savings package are sweeping cuts to the runaway National Disability Insurance Scheme, which will save $37.8 billion over the five years from 2025/26, with program spending falling from $56.1 billion in 2026/27 to $55.1 billion the following year.

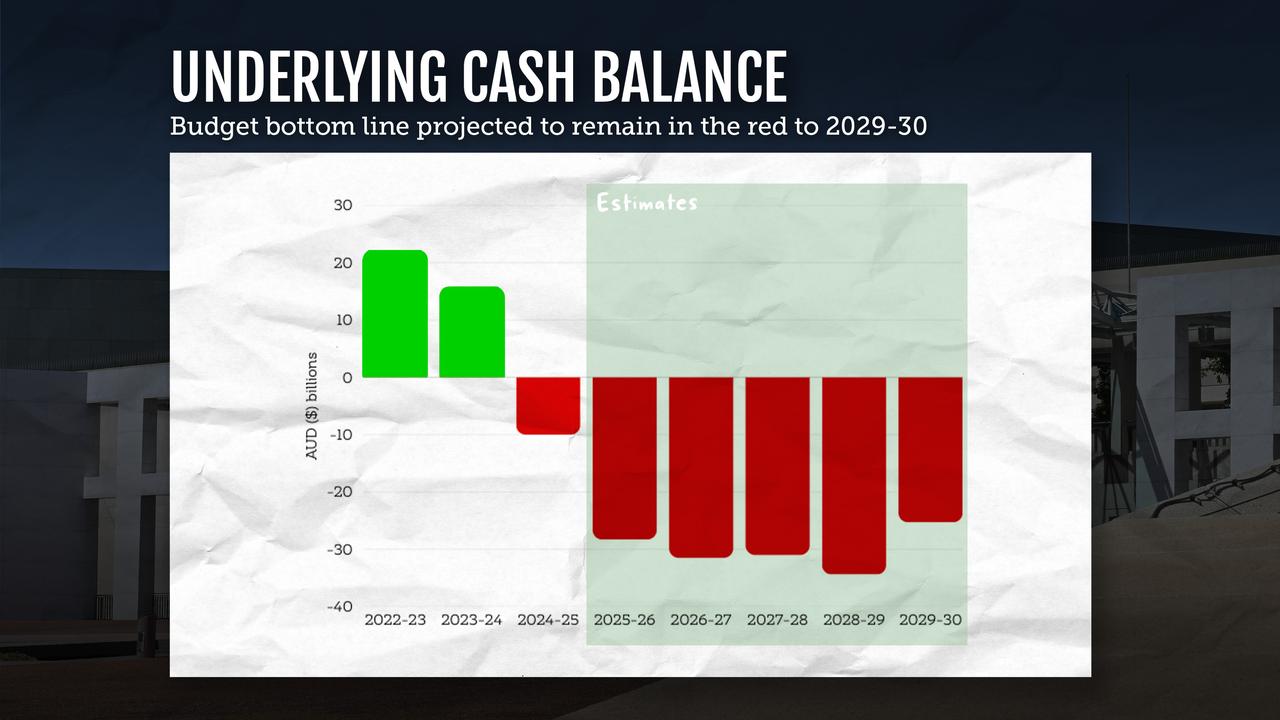

Despite the underlying budget deficit improving by $8.5 billion since the December mid-year update to $28.3 billion in 2025/26, the fiscal bottom line is projected to remain in the red until 2034/35.

This is a year earlier than the previous budget forecast, largely as a result of the NDIS reforms.

But aged care, defence and hospital payments to the states are expected to grow faster over the medium term than they were projected to in December.

However, “off-budget” spending continued to increase, with the headline deficit climbing from $47.9 billion this financial year to $64.1 billion in 2026/27.

The government’s net policy decisions since December improved the cumulative bottom line by $8.2 billion, but most of the improvement is projected to happen in 2029/30.

Government decisions, including $2.55 billion for fuel excise cuts, are estimated to make the deficit $5.3 billion worse off in 2025/26 and $6.5 billion worse off in 2026/27.

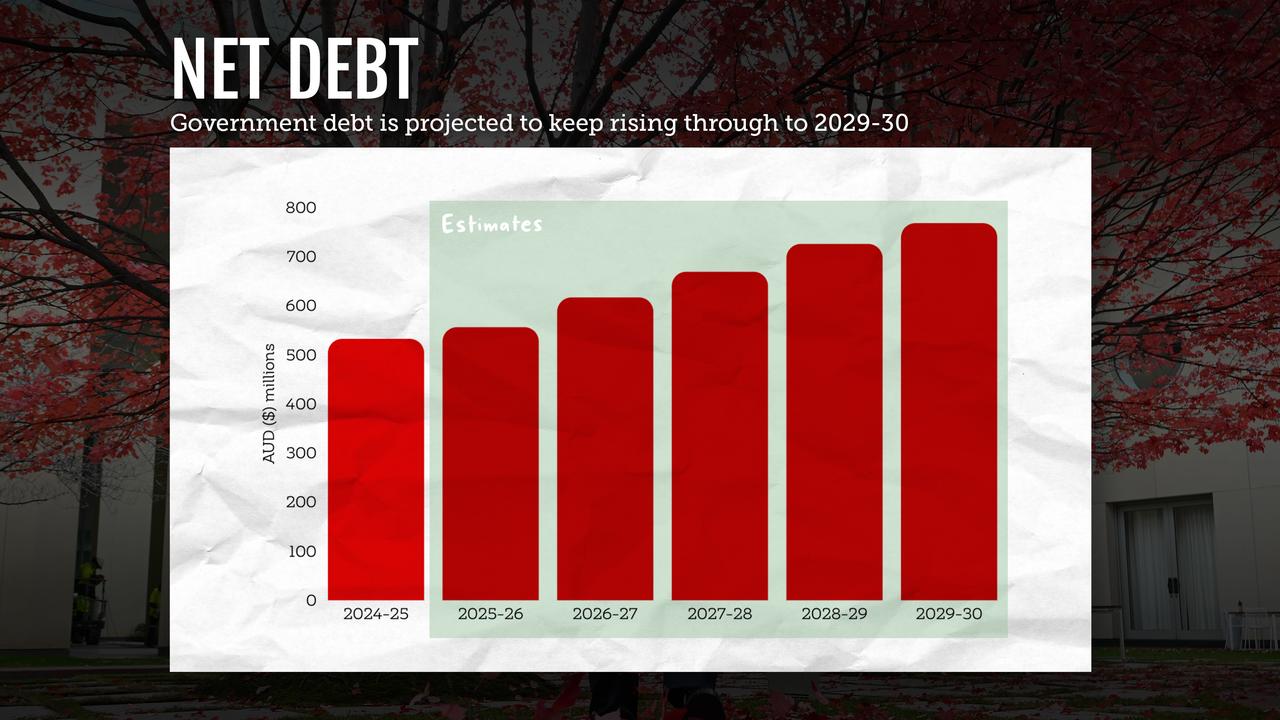

Gross debt is expected to finally exceed $1 trillion in 2026-27, while net debt is expected to hit $616 billion, or just under one fifth of GDP.