There is a storm brewing to blow up the Federal Government’s Compensation Scheme of Last Resort. Michael Pascoe reports an unknown factor in forecasting the outcome is whether the responsible minister is playing a sophisticated political game or is a mug about to make a bad situation worse.

Is Assistant Treasurer Danny Mulino a canny politician and smart economist with a Yale PhD or Richard Marles’ little factional mate upjumped from Victorian State Parliament?

That will be decided by how he fixes or makes worse the government’s Compensation Scheme of Last Resort (CSLR) and the Australian Financial Complaints Authority (AFCA) that drives it.

By raising the possibility of using your superannuation fund to compensate people who make dud financial decisions he is either seeding the clouds for the impetus to make major reforms or he’s displaying a tin ear and a penchant for being generous with other people’s money.

Pilloried from Left and Right

Mulino’s suggestion of adding superannuation funds to the list of entities levied to compensate punters has been immediately pilloried from left and right, most obviously by the trade unions and super industry itself.

The AFR’s John Kehoe highlights ($) the moral hazard of consumers having their riskier investments underwritten by innocent parties with CSLR levies heading towards $300 million this year, the vast majority of it to be paid by honest financial advisers.

Crikey’s Glenn Dyer and Bernard Keane point to the injustice of those with substantial assets being over-represented in the compensation queue as they’re more likely to pursue higher and therefore more risky returns.

Super milk cow

“Mulino is suffering from Chalmers’ problem of regarding the superannuation sector as just another resource for government to raid to fix problems elsewhere. There is no proposal to adjust the tax treatment of super — the government has had enough of that after its back-down on changes a couple of months ago — but simply to take money from members, via their funds, to compensate victims of a different part of the finance industry.”

The Stockbrokers and Investment Advisers Association sees the series of special levies becoming so steep it will prevent new advisers joining the industry that is already short of responsible advice.

As it stands, the CSLR is unsustainable, damaging good financial advisers, penalising the innocent and ignoring the dodgy.

The AFCA sees itself as the Tooth Fairy,

happily sticking folding money under the pillows of kiddies’ and some old codgers with gold-inlaid dentures in a glass beside the bed as well.

CLSR a ‘money pit’

Established with good intent to help folk who have lost money by following bad financial advice, the CSLR has morphed into a money pit as the claims have rolled in to kind-hearted AFCA. It’s a bit of a mini-NDIS except the funding is coming from some of the good players in the financial system, instead of taxpayers.

Note, only “some”. Arguably the main sources of losses are the dodgy management investment schemes (MIS) that have thrived for many decades while lightly, belatedly and only occasionally regulated by our notorious financial watchpuppy, ASIC.

Whether joke tree plantations or too-good-to-be-true superannuation investments, MIS have been the vehicle of choice for the ripoff merchants. But MIS issuers and the so-called “responsible entities” do not contribute to the compensation fund.

MIS the devil’s playground

Financial advisers, credit providers (banks), credit intermediaries (brokers) and securities dealers (stockbrokers) do, but not anyone wanting to set up a MIS and take the punters’ money.

Funny thing that. Logic, equity and history would have MIS issuers and ASIC itself kicking into the compo can.

I’ll come back to ASIC but if you wonder why re the former, ask the Financial Services Council as it is about the only mob to think otherwise. The FSC is mainly known for its unceasing campaign against industry super funds and being Andrew Bragg’s old school. It has long enjoyed a close relationship, shall we say, with the Liberal Party.

There’s nothing new about MIS being the financial devil’s playground. Provide a loophole, or a gaping chasm, and the shonks will make use of it. A dozen years ago, the Corporations and Markets Advisory Committee (CAMAC) conducted a lengthy inquiry into reforming the MIS framework but the FSC didn’t like it, thinking a little more regulation and oversight would be, you know, “regulatory burden”.

Bitter harvest

One of the minor line items in the Abbott government’s first budget was to scrap CAMAC.

In the long and painful aftermath of multiple crooked or incredibly inept agricultural schemes imploding, the Senate economics committee in 2016 delivered its “Bitter Harvest” report with plenty of criticism of the MIS system and ASIC’s frequent failures.

And Mulino’s predecessor, Stephen Jones, launched an MIS regulatory framework review that managed to come up with a consultation paper two years ago but since then, nada.

A common feature of just about every financial scandal has been ASIC being asleep at the wheel. Whether it was the agri MIS marketed with “ASIC approved” on the cover or Storm Financial given the all clear by ASIC despite comprehensive briefing on the disaster about to happen, the watchpuppy characteristically doesn’t move until it’s all over bar the crying.

First Guardian and Shield failures

And so it is again with the billion-dollar First Guardian and Shield failures. ASIC was tipped off when the scam was in its infancy and did nothing. Incredibly, ASIC advised Macquarie that Shield was dodgy but didn’t extend the same warning to another platform provider, Equity Trustees, allowing a further $160 million to be sunk in the scheme.

Now ASIC has been trying to big note itself over its investigation but is fooling nobody.

And it keeps coming, as these pages reported last week. The relevant shadow minister, Pat Conaghan, gave ASIC both barrels on Wednesday, suggesting

we need ASIC reform rather than law reform.

If one was looking for someone to make good, it makes more sense to bill the watchpuppy for losses incurred after it failed to act than to penalise the innocent players trying to do the right thing in the advice space. (And ASIC makes hundreds of millions of dollars in fees each year for the Federal Government.)

That is where the collateral damage is occurring now from the existing compo scheme. The extent of losses initially from Dixon Advisory’s dud recommendations and at a higher level again now from First Guardian and Shield means

levies on advisers are becoming punitive and threatening to close advice down.

Hence Mulino looking for someone else to pay, i.e. your super fund, or using the backlash from that proposal as the excuse for overhauling the compo system.

As it stands, the maximum individual payout from CSLR is $150,000, but there are a lot of individuals sticking their hands up.

AFCA’s dreaded ‘But For’ clause

The system is made worse by AFCA introducing its simply unbelievable “but for” rule in the Dixon aftermath. In the authority’s own words:

“In circumstances where a complaint is about financial advice related to a MIS that may have subsequently failed (and is no longer an AFCA member), we will consider whether the advisor breached their legal obligations and if they did so, we will consider ‘but for’ the breach what would the complainant have invested in.”

So there isn’t just compensation for the loss of capital from being led to make a bad decision,

AFCA wants to give you the profit you might have made by doing something smart with your money.

It’s only a slight exaggeration to say it’s like me being robbed of $20, money that I might have bought a winning OzLotto ticket with and thus I should receive the maximum $150,000 compensation from CSLR.

It is all a complicated mess with the Law of Unintended Consequences hard at work, as usual. Whether Mulino has what it takes to improve or worsen the mess is to be seen.

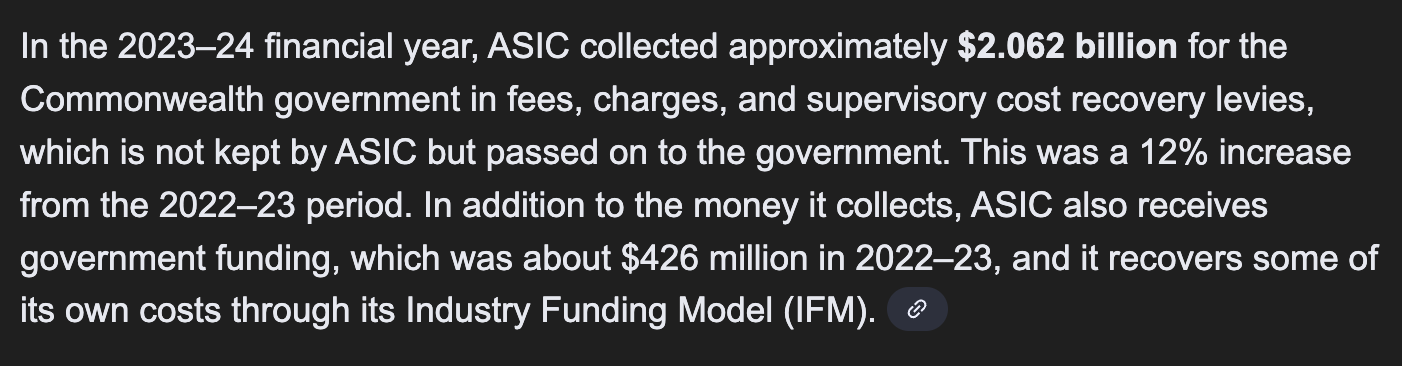

Editor’s Note: maybe tapping ASIC would do the trick. They rake in $2B in fees for the Federal Government, which funds them to the tune of $430m pa. Having to fund losses from crooks and incompetents might be an incentive for better regulation.